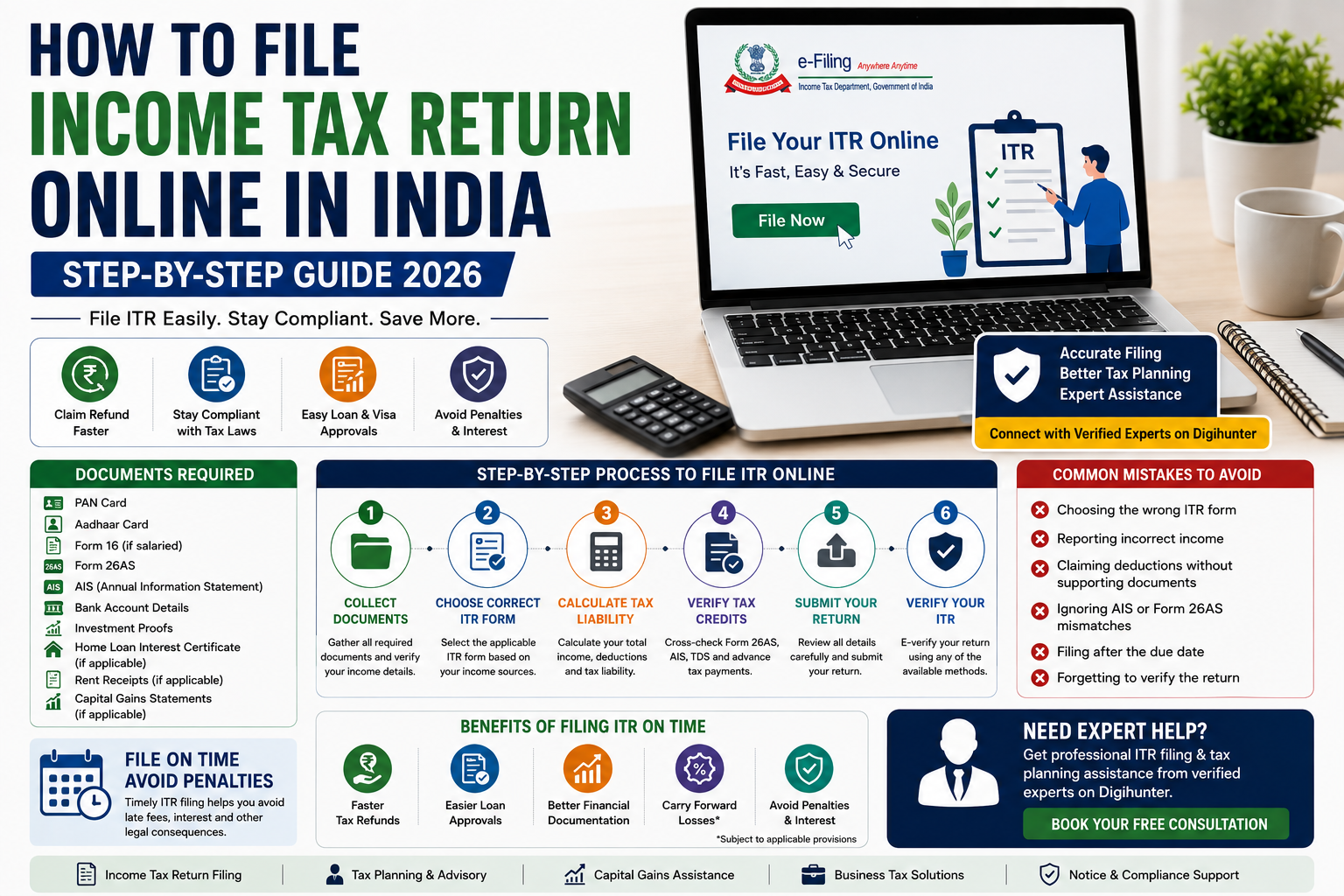

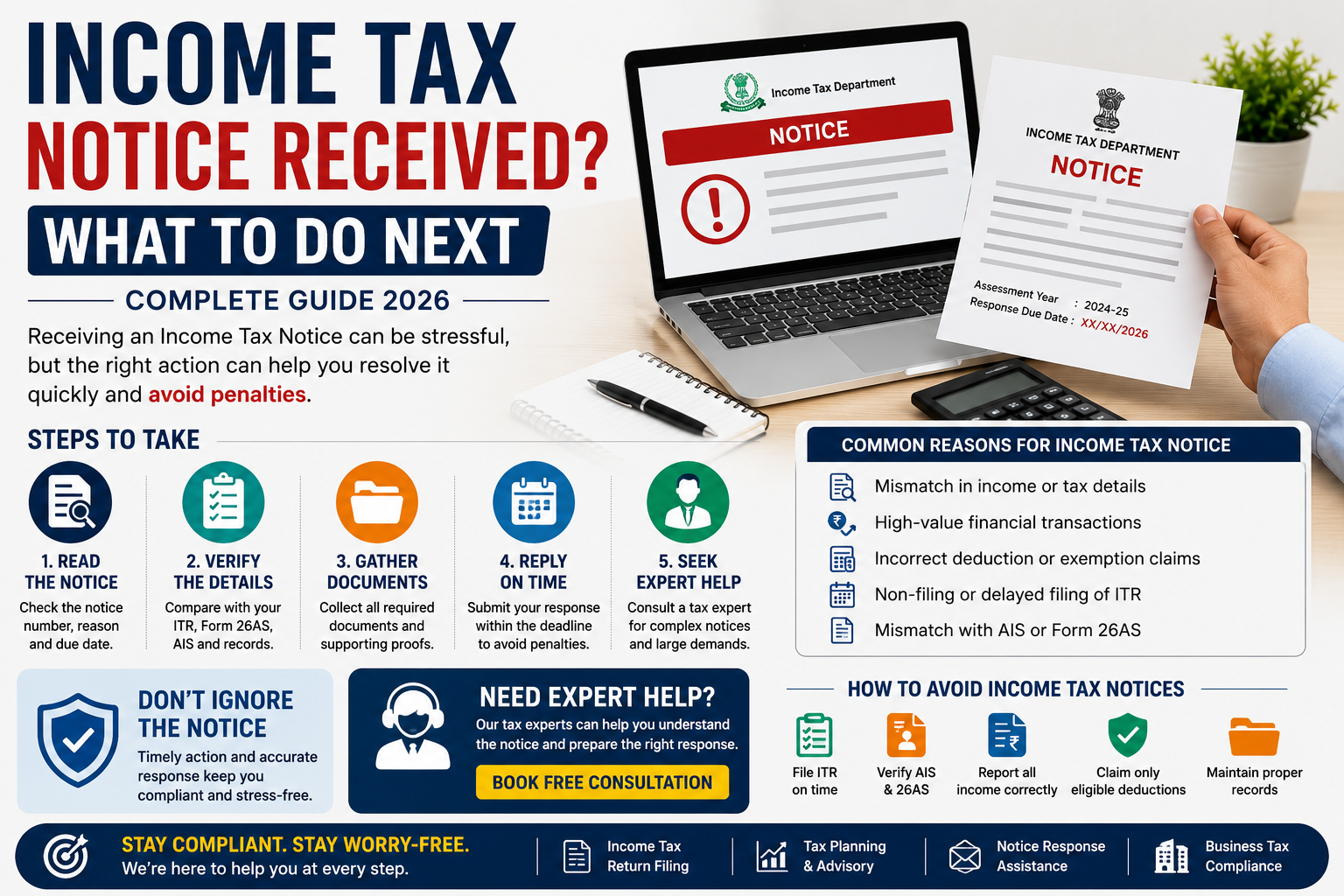

How to File Income Tax Return Online in India (Step-by-Step Guide 2026)

Filing your Income Tax Return (ITR) is one of the most important financial responsibilities for taxpayers in India. Whether you are a salaried employee, freelancer, business owner, or professional, filing your ITR on time helps you remain compliant with tax laws, claim refunds, and avoid penalties.

This guide explains the step-by-step process to file an Income Tax Return online in 2026, the documents required, common mistakes to avoid, and why professional assistance can make the process easier.

What is an Income Tax Return (ITR)?

An Income Tax Return (ITR) is a form submitted to the Income Tax Department that reports your:

● Income earned during the financial year

● Taxes paid

● Deductions and exemptions claimed

● Tax liability or refund.

Filing your ITR correctly helps maintain a clean financial record and is often required for loans, visa applications, and financial transactions.

Who Should File an ITR?

You should consider filing an Income Tax Return if you:

● Have taxable income under the applicable tax rules.

● Want to claim a refund of excess TDS deducted.

● Have capital gains from property, shares, or mutual funds.

● Earn income from business or professional services.

● Meet other filing requirements prescribed under the Income Tax Act.

Eligibility and filing requirements may vary based on the applicable assessment year and current tax provisions.

Documents Required for ITR Filing

Keep these documents ready:

● PAN Card

● Aadhaar Card

● Form 16 (for salaried employees)

● Form 26AS

● Annual Information Statement (AIS)

● Bank account details

● Investment proofs

● Home loan interest certificate (if applicable)

● Rent receipts (if applicable)

● Capital gains statements (if applicable)

Step-by-Step Process to File ITR Online

Collect Required Documents

Choose the Correct ITR Form

Calculate Your Tax Liability

Verify Tax Credits

Submit Your Return

Verify Your ITR

Want to file your ITR without errors?

Connect with verified tax professionals through Digihunter for accurate Income Taxa Return filing and expert tax planning.

Common Mistakes to Avoid

❌ Choosing the wrong ITR form

❌ Reporting incorrect income

❌ Claiming deductions without supporting documents

❌ Ignoring AIS or Form 26AS mismatches

❌ Filing after the due date

❌ Forgetting to verify the return

Benefits of Filing ITR on Time

✔ Faster tax refunds

✔ Easier loan approvals

✔ Better financial documentation

✔ Avoid penalties and interest

✔ Carry forward eligible losses (subject to applicable provisions)

Conclusion

Filing your Income Tax Return accurately and on time helps you stay compliant, claim eligible refunds, and maintain a strong financial record. By keeping the required documents ready, verifying your tax information, and avoiding common mistakes, you can make the filing process smooth and hassle-free.

If your tax situation is complex, consulting a qualified professional can help ensure accurate filing and better tax planning.

Need expert tax planning assistance? Connect with verified professionals via Digihunter today.

✔ Income Tax Return Filing

✔ Tax Planning

✔ Capital Gains Tax Assistance

✔ Business Tax Advisory

Protect your family financially

Protect your family financially For expert help, explore

For expert help, explore